Conducting a Series Analysis

- Overview

- Displaying an Analysis for a Time Series

- Basic Analyses

- Stationarity Analyses

- Autocorrelation Analyses

- Decomposition Analyses

- Seasonal Adjustment Analyses

- Seasonal Adjustment Formulas

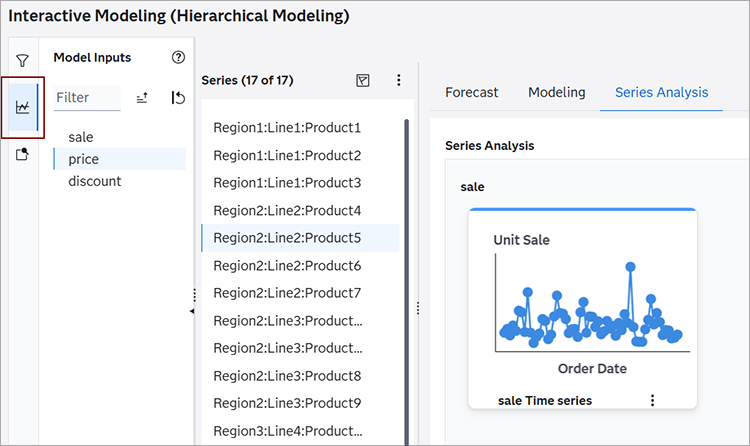

From the Series Analysis tab in Interactive Modeling, you can display plots for any time seriesan aggregation of transactional data into specified time intervals and sorted according to unique combinations of the default attributes (BY variables) selected from the Series pane. For each time series, you can view plots for the dependent variable or any independent variable.

Overview

When you first select the Series Analysis tab, the right pane shows a time series plot of the dependent variable for the item that is selected in the Series pane. For time series analysis, only one item can be selected at a time.

The analyses are placed on a row for each model

input. You can add more rows for each model input. If you add a model input that is

already

placed in the right pane, the input is added again with a number appended to the variable

name. For example, if you have already placed a model input on the canvas with the

name

Quantity, adding it again puts the input on the

canvas with this name:

Quantity (1)

For most analyses, you can add only one type for each input row. For analyses that can be modified, you can add several of these types to an input row if you change the default settings.

When you close a session in Interactive Modeling, the analyses that you have arranged are preserved for you. The next time you open Interactive Modeling and select the Series Analysis tab, the plots and graphs that you have arranged in the middle pane remain in place.

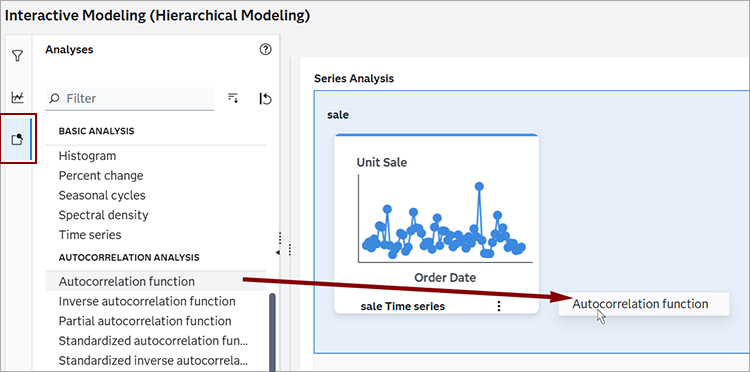

Displaying an Analysis for a Time Series

Follow these steps to display a plot for a time series.

- From the Series

Analysis tab in Interactive Modeling, select an item in the

Series pane.

The plot for the selected time series is generated and displayed on the canvas in the Series Analysis tab.

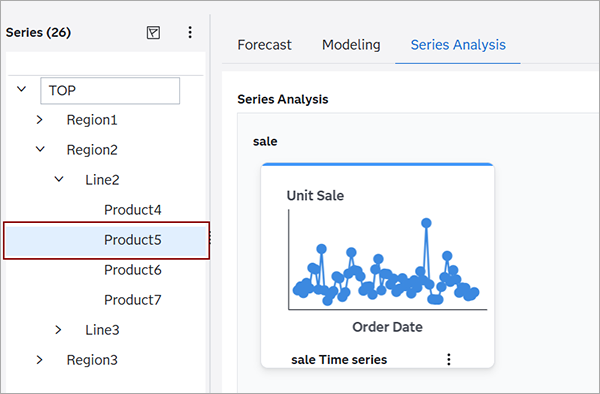

If Hierarchical Modeling is turned on, the Series pane shows the time series in a tree view.

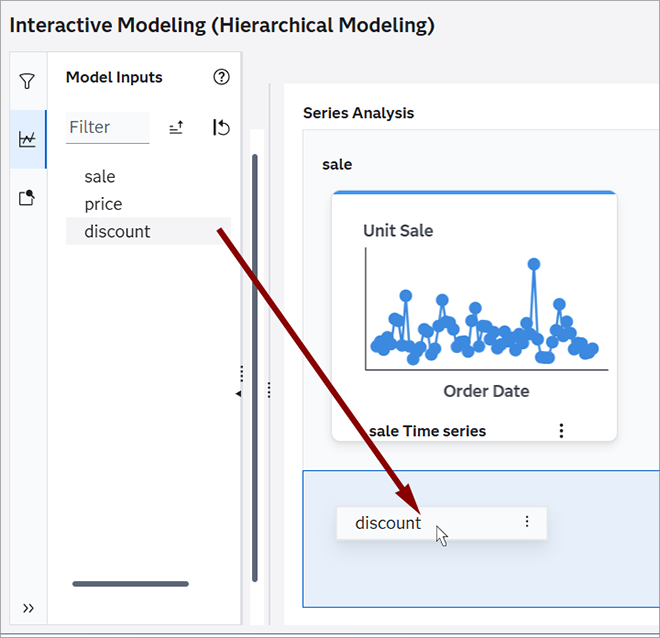

- Place an input variable in the canvas in the

right pane.

- Select

in the left pane.

in the left pane.

The dependent variable and independent variables for the project are displayed in the Model Inputs pane.

- Select one or more of the input variables

in the left pane and drag it to the canvas.

A row is added for each model input in the right pane. A time series plot is displayed by default.

As you add input variables to the canvas, each input is placed in a new row. You can drag and drop each row on the canvas to reorder them. You can also reorder the inputs by clicking

in the top right corner of the canvas and selecting Reorder

Analyses.

in the top right corner of the canvas and selecting Reorder

Analyses.You can remove a row from the right pane by clicking

in the top right corner of the row and selecting

Remove. The initial row for the dependent variable cannot be

removed. - Select

- Select an analysis to be displayed using one

of these methods.

- Select

in the left pane and drag an analysis to the row for the model input.

You can select multiple analyses, but, for each input row, you can add only one type

of each analysis

in the left pane and drag an analysis to the row for the model input.

You can select multiple analyses, but, for each input row, you can add only one type

of each analysis

- Select an analysis from the drop-down menu

in the row for the model input.

The plot for the selected analysis is generated and displayed in the tile.

At the bottom right corner of the input tile is a menu icon:

. The menu provides these options.- Open

-

Displays a window with a larger view of the plot.

- Settings

-

Use this option to change settings for certain settings, such as Lag or Decomposition method. Settings are not available for all of the analyses.

- Log

-

If there is an error generating the plot, this option enables you to open and download the log to determine the cause of the error. The log option is not shown if the plot is generated successfully.

- Remove

-

Removes the analysis from the model input row. The Time Series cannot be removed from the model input row.

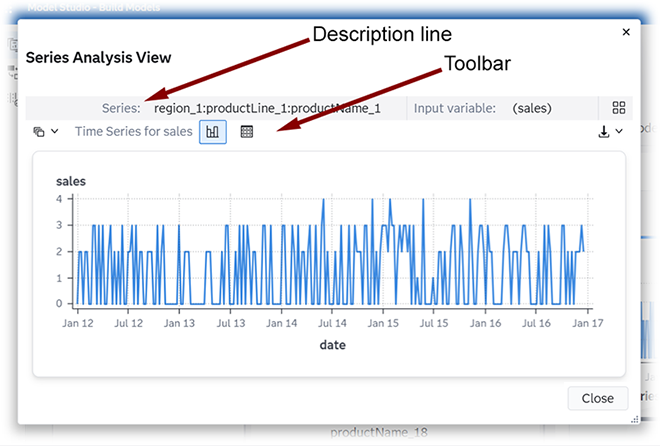

- Select

- Click and select Open. A larger plot is displayed in a

new window.

There is a

description lineat the top of the window showing the Series, which indicates the combination of BY variables for this time series. The line also shows the name of the Input variable and the icon, which adds all of the analyses in the row to the

window.

icon, which adds all of the analyses in the row to the

window.Below the

description line, there is a toolbar with these actions. ─ Displays a list of all of the analyses in this row. You can select

another analysis to display it in this window.

─ Displays a list of all of the analyses in this row. You can select

another analysis to display it in this window. ─ Shows the plot for the analysis. This is the default. You can show

the plot, the table, or both in this window.

─ Shows the plot for the analysis. This is the default. You can show

the plot, the table, or both in this window. ─ Shows the table for the analysis. You can show the plot, the table,

or both in this window.

─ Shows the table for the analysis. You can show the plot, the table,

or both in this window. ─ Displays two options for downloading the data to your local drive.

You can download Raw data or Formatted

data.

─ Displays two options for downloading the data to your local drive.

You can download Raw data or Formatted

data.- ─ Use this menu to open the Settings or the Log for the analysis. The

Settings option is available only for analyses that have a

Lag or Decomposition method that can

be changed.

- Click . You are prompted to save data for the table or graph that is displayed.

If both are displayed, you are prompted to save data for both. The data is downloaded

as a

CSV file.

For Time Series, the data downloaded for the plot and table are the same.

For Histogram and Seasonal cycles, the plot data that is downloaded is different from the table. The data downloaded for the table provides the descriptive statistics for the time series. The data downloaded for the plot provides the values in the GTML that is used to create the plot.

- Click at the top right corner of the model input row. This opens all of the

analyses in the row in an enlarged window. This icon is also available when you open

the

enlarged view for a single analysis.

The view of multiple analyses provides this icon:

. Clicking this icon opens the Display Settings

window, which you can use to add more analyses to the window. This action also adds

the

analysis to the model input row.

. Clicking this icon opens the Display Settings

window, which you can use to add more analyses to the window. This action also adds

the

analysis to the model input row.

Basic Analyses

The following basic analyses are available.

|

Time series Displays a plot of the selected time series over the historical time period |

|

|

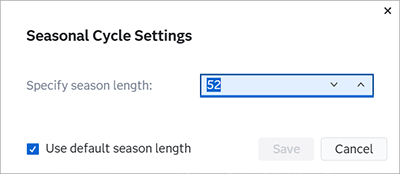

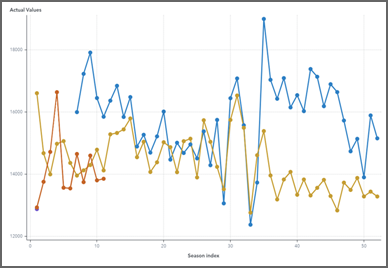

Seasonal cycles Displays any seasonal patterns for the selected time series at regular intervals in the plot You can change the seasonality (length of the season) for this plot to investigate different seasonal patterns. Using different seasonality specifications enables you to add multiple seasonal cycles to the canvas and compare the different plots. You cannot add a seasonal cycle to the canvas using the same season length as one that is already on the canvas. To change the seasonal cycle length,

click

If you click View Details, you can also change the seasonal cycle length in the larger view of the plot using the menu icon in the upper right corner. |

|

|

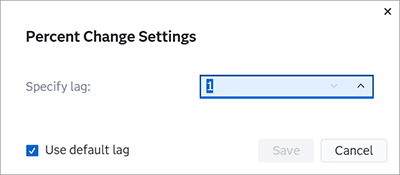

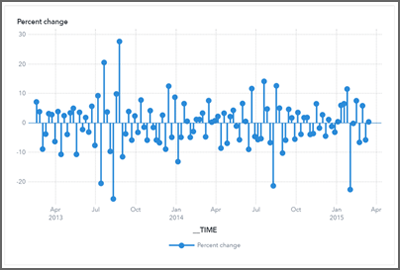

Percent change Displays the percent difference between each time period for the selected time series You can change the number of lags for which the change is shown in the time line. By default, each change shows the percent difference from the previous measurement (lag=1). For example, for monthly data (interval=month), for the default lag of 1, the first measurement on the plot starts at the second month and shows the percent difference from the prior month. However, if you change the lag to 3, then the first measurement on the plot starts at the fourth month and shows the percent difference from three months before. Changing the default lag specification enables you to add more percent change plots to the canvas for comparison. To change the lag specification, click

If you click View Details, you can also change the lag specification in the larger view of the plot using the menu icon in the upper right corner. |

|

|

Histogram Displays a series of columns representing the frequency of the selected time series |

|

|

Spectral Density Shows the periodogram and the estimate of the spectral density of the selected time series. |

|

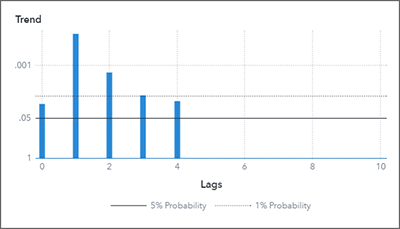

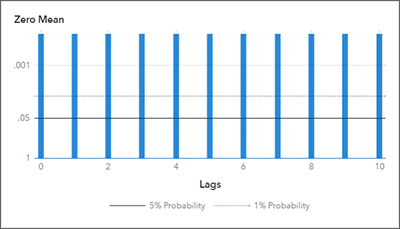

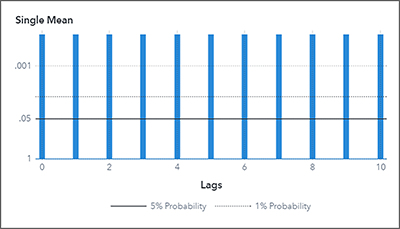

Stationarity Analyses

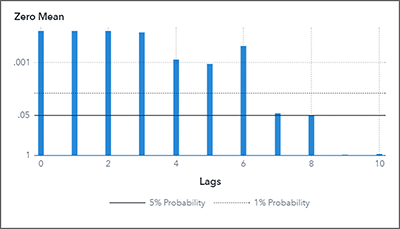

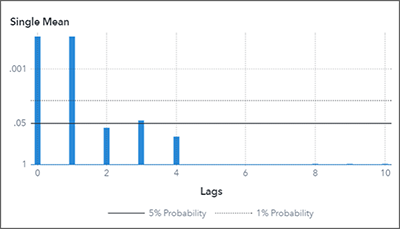

These plots are used to test zero-mean stationarity, single-mean stationarity, and linear-time trend stationarity. For zero-mean stationarity, a unit root test is conducted for an AR(p) model with zero mean for different values of lag p. For single-mean stationarity, a unit root test is conducted for an AR(p) model with a nonzero mean for different values of lag p. For trend stationarity, a unit root test is conducted for an AR(p) model with linear-time trend for different values of lag p.

If seasonality for the time series is d and 2<= d <= 12, then seasonal unit root tests are conducted for zero-mean and single-mean AR(p)(d) models for different values of lag p.

For more information, see Stationarity Tests and PROBDF Function for Dickey-Fuller Tests in the SAS/ETS User's Guide.

Each plot shows the logarithm of significance probabilities for unit root tests for different lag values p. The plots show log scale formats. The plot CSV file contains the raw values for the plot. There is a difference between the values in the plot CSV file and the values that are displayed when you hover over the plot. The following stationarity analyses are available.

|

|

|

|

|

|

|

|

|

|

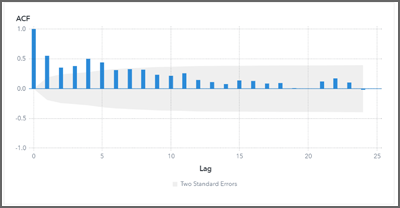

Autocorrelation Analyses

The following autocorrelation analyses are available.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

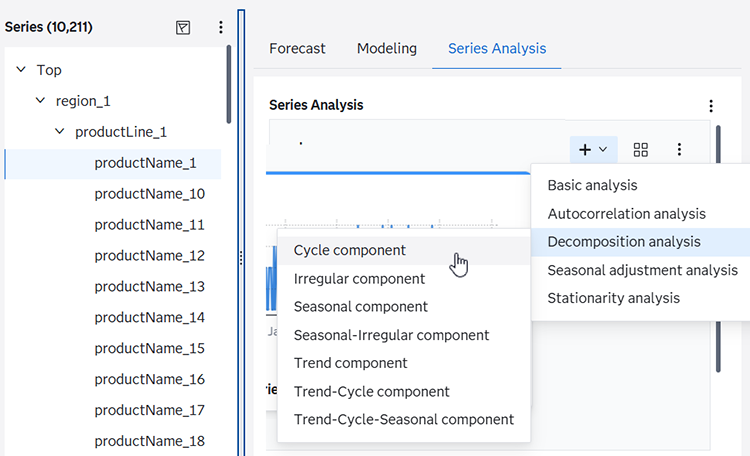

Decomposition Analyses

You can generate decomposition analyses for the model inputs. Classic decomposition breaks the time series into the following components.

- Trend

- Cycle

- Seasonal

- Seasonal-irregular

- Trend-cycle

- Trend-cycle-seasonal

Decomposition analysis is performed when the seasonality is greater than or equal to 2. If seasonality is less than 2, an error is generated.

The decomposition method determines the mode of

the decomposition to be performed. There are four decomposition methods: additive,

log-additive, pseudo-additive, and multiplicative. After you add a decomposition analysis

to

the canvas in Series Analysis, click on the analysis tile and select Settings. Select

from one of the following methods.

- Additive

-

specifies additive decomposition.

- Log-additive

-

specifies log-additive decomposition. This method requires strictly positive time series. If this method is selected and the time series contains any nonpositive values, an error is generated.

- Multiplicative

-

specifies multiplicative decomposition. This method requires strictly positive time series. If this method is selected and the time series contains any nonpositive values, an error is generated.

- Pseudo-additive

-

specifies pseudo-additive decomposition. This method requires a nonnegative-valued time series. If the accumulated time series contains negative values, selecting the pseudo-additive method generates an error.

- Automatic (default).

-

specifies multiplicative decomposition when the accumulated time series contains only positive values, pseudo-additive decomposition when the accumulated time series contains only nonnegative values, and additive decomposition under other circumstances. This method is selected by default.

The following decomposition analyses are available.

|

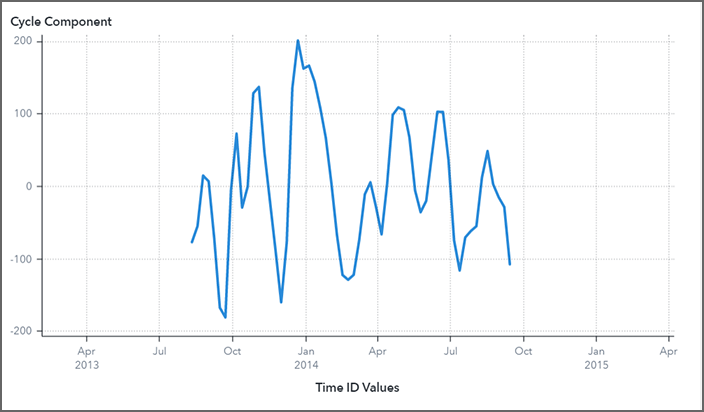

Cycle component Displays the cycle component for the selected time series. The cycle component is obtained by subtracting the trend component from trend-cycle component. The Y axis shows a scaled-down measurement of the actual values. |

|

|

Irregular component Displays the irregular component for the selected time series. The irregular component is computed by using the seasonal-irregular component and the seasonal component. The Y axis shows a scaled-down representation of the actual values. |

|

|

Seasonal component Displays the seasonal component for the selected time series. The seasonal component is obtained by averaging the seasonal-irregular component for each season. The Y axis shows a scaled down representation of the actual values. |

|

|

Seasonal-Irregular component Displays both the original series and the seasonal-irregular component for the selected time series. The seasonal-irregular component is computed by using the original series and the trend-cycle component. The Y axis shows a scaled-down representation of the actual values. |

|

|

Trend component Displays both the original series and the trend component for the selected time series. The cycle component is obtained by subtracting the trend component from the trend-cycle component. The Y axis shows the actual values for the time series. |

|

|

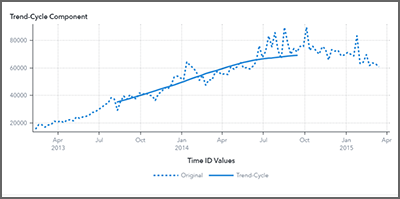

Trend-Cycle component Displays both the original series and the trend-cycle component for the selected time series. The trend-cycle component is computed from the centered moving average for the s-period. The Y axis shows the actual values for the time series. |

|

|

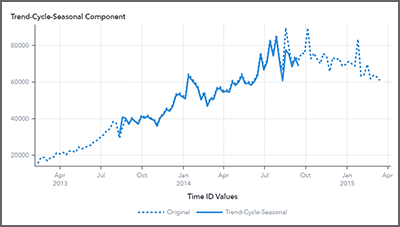

Trend-Cycle-Seasonal Component Displays both the original series and the trend-cycle-seasonal component for the selected time series. The trend-cycle-seasonal component is computed from the original series and the irregular component. The Y axis shows the actual values for the time series. |

|

Seasonal Adjustment Analyses

You can generate seasonal adjustment analyses for the model inputs. The following seasonal adjustment analyses are available.

|

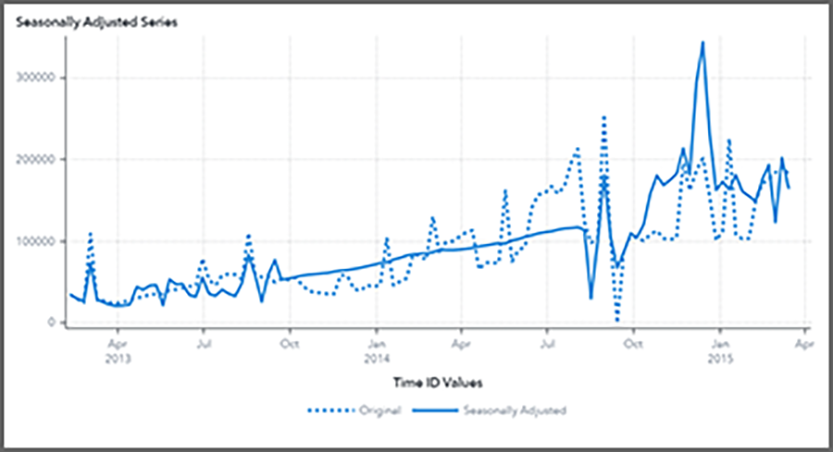

Seasonally adjusted series Displays both the selected time series and its seasonally adjusted series. The seasonally adjusted series is computed from the trend-cycle component and the irregular component. The Y axis shows the actual values for the time series. |

|

|

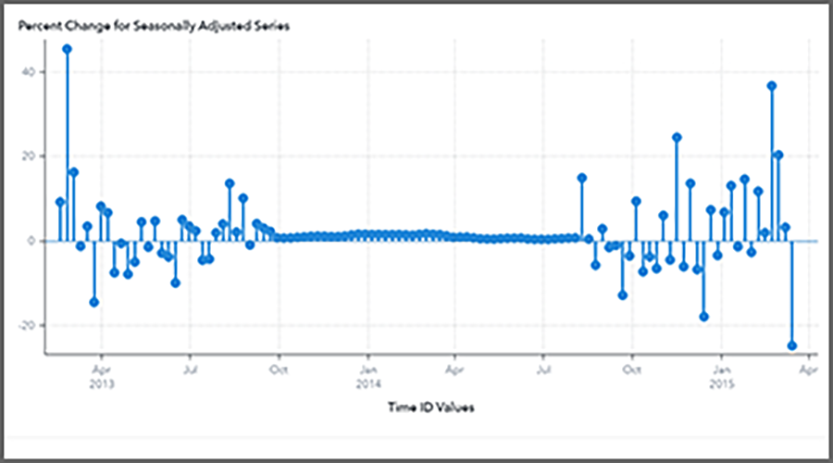

Percent change for seasonally adjusted series Displays the percent difference between each time period for the seasonally

adjusted series of the selected time series. The time period is set by the seasonality for the time interval and the lag. The default for lag is 1, but

you can change it by clicking See Seasonality to determine the seasonality based on the time interval set for the time variable. |

|

Seasonal Adjustment Formulas

|

Component |

Decomposition Method |

Formula |

|---|---|---|

|

original series |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

trend-cycle component |

multiplicative |

centered moving average of Ot |

|

additive |

centered moving average of Ot |

|

|

log-additive |

centered moving average of |

|

|

pseudo-additive |

centered moving average of Ot |

|

|

seasonal-irregular component |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

seasonal component |

multiplicative |

seasonal Averages of SIt |

|

additive |

seasonal Averages of SIt |

|

|

log-additive |

seasonal Averages of SIt |

|

|

pseudo-additive |

seasonal Averages of SIt |

|

|

irregular component |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

trend-cycle-seasonal component |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

trend component |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

cycle component |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

|

|

seasonally adjusted series |

multiplicative |

|

|

additive |

|

|

|

log-additive |

|

|

|

pseudo-additive |

|

The trend-cycle component is computed from the centered moving average for the s-period as follows:

The seasonal component is obtained by averaging

the seasonal-irregular component for each season where  and

and  .

.

The seasonal components are normalized to sum to one (multiplicative) or zero (additive).

See Also

-

Generating Output from SAS Model Studio in SAS Visual Forecasting: Overview